Healthspan Wealth · Enterprise thesis

The prize is enterprise. The path is not.

We should sell into scaled operating RIAs before the SEIA track defines the company.

92tight SEIA-neighborhood firms

1,787scaled $5B-$100B firms

4explicit Salesforce FSC signals in our stack scan

June 25, 2026

Argument 1

The market and the economics are the same argument.

Read: the SEIA-like pool is useful for requirements, but the economics require a broader operating-RIA motion.

Argument 2

Grimes is the more usable version of the SEIA problem.

| Firm | Scale | Motion |

|---|---|---|

| Grimes | $6.3B AUM ~69 employees | Operator-led app/discovery motion |

| SEIA | $22.5B ADV / $30B+ AUA ~230-251 employees | Enterprise alignment and procurement |

Read: Grimes is not smaller as a compromise. It is smaller as a route into motion.

Argument 3

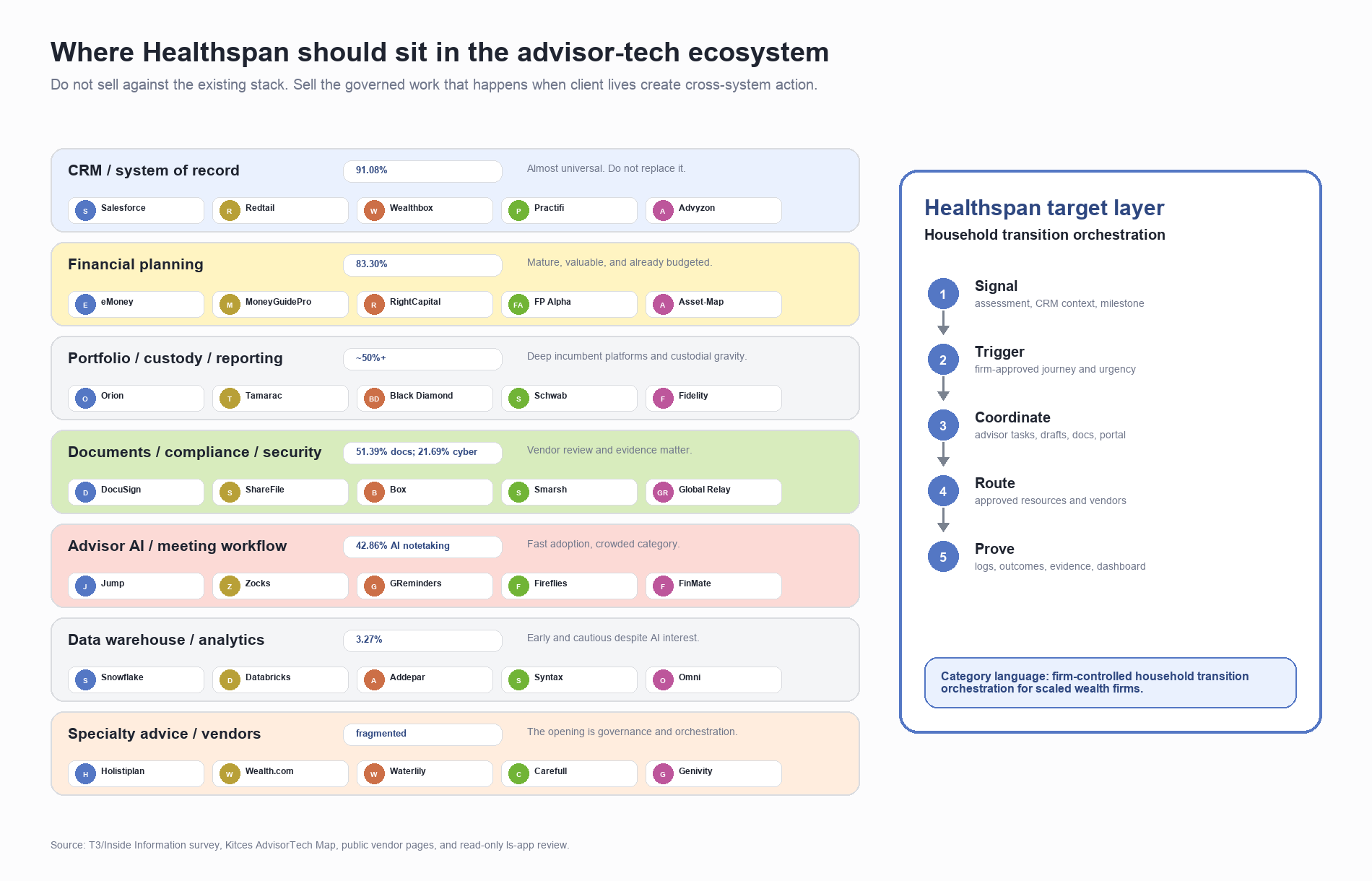

CRM is a lane. The company has to own action across lanes.

Read: Salesforce matters. Salesforce alone is not enough.

Conclusion